This week, we look at red flags while investing, the US housing market, Peloton, Henry Singleton, Insurance Float (a.k.a. other people's money), FinTech vs. traditional banks

This migration to lower-cost areas may lead to lower workforce participation. For many families Redfin has relocated, the money saved on housing costs lets one parent stop working. A wave of Redfin customers are retiring early.

It’s not just income that’s k-shaped, but mobility. 90% of people earning $100,000+ per year expect to be able to work virtually, compared to 10% of those earning $40,000 or less per year. The folks who need low-cost housing the most have the least flexibility to move.

It’s all about that community they have built coupled with the superior user experience.

Peloton has a very profitable business model (outstanding unit economics) and some people fear that competitors may replicate its success. While the hardware is easier to copy (a bike with a tablet attached), software and a vertically integrated user experience are harder to replicate.

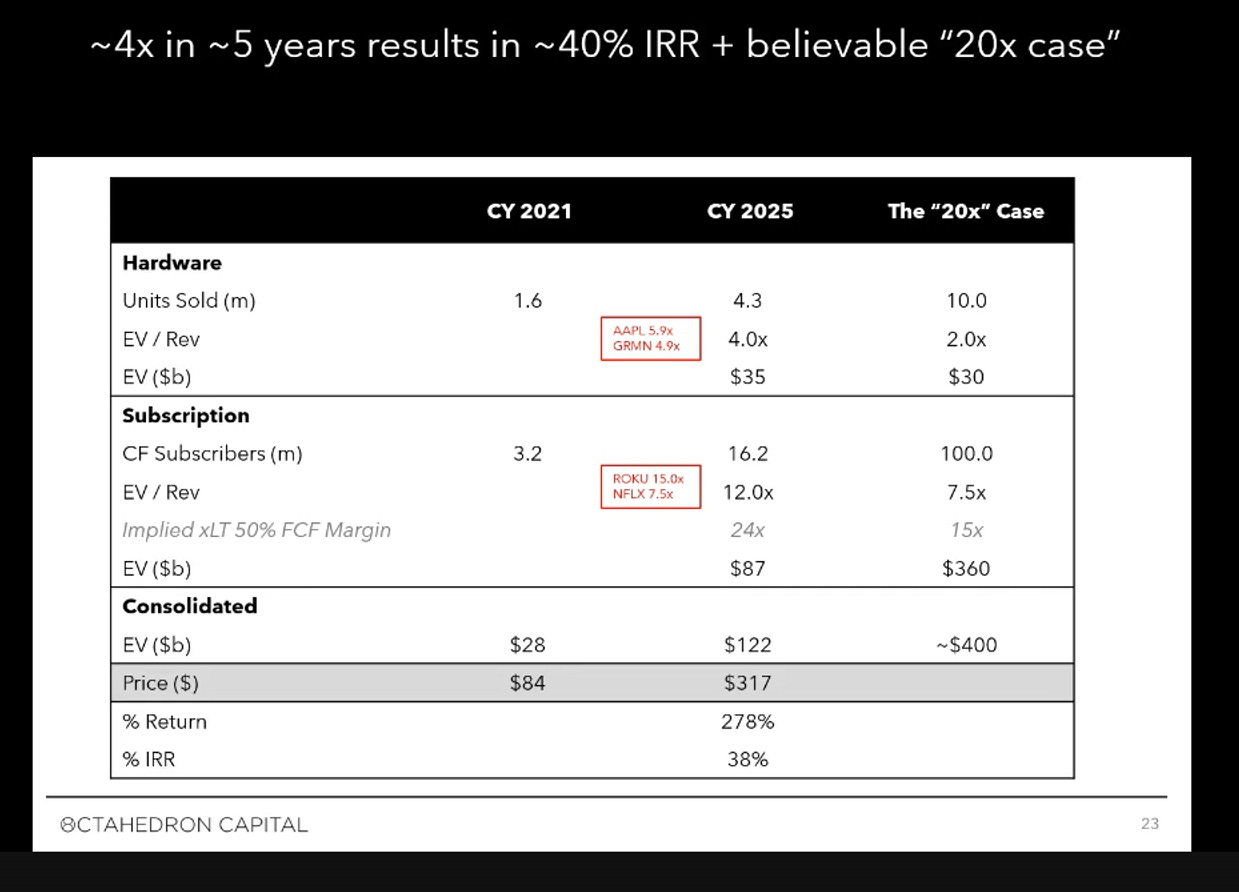

Read this with Ram Parameswaran’s pitch at Sohn Investment Conference 2021 and you can understand how this company has a huge upside attached to it.

Long read on Singleton, who ran Teledyne for several years and his capital allocation skill.

I don’t believe all this nonsense about market timing. Just buy very good value, and when the market is ready, that value will be recognized.

Buffett, on Singleton: the failure of business schools to study men like Singleton is a crime. Instead, business schools hold up as models executives cut from a McKinsey & Co. cookie cutter.

By 1967, Buffett’s eye had been turned by National Indemnity, headquartered a few blocks away from his office in Omaha. After a fifteen minute meeting with its founder, he agreed to buy the whole company for $8.6 million, a $1.9 million premium over its net worth. Rather than buy it directly in the fund, he bought it out of Berkshire Hathaway. The acquisition handed Buffett a new investment portfolio to manage. Its portfolio had previously been managed by its founder who, according to Alice Schroeder in her book, Snowball, “carried around hundreds of stock certificates in an old gym bag.” In 1967, the portfolio was sitting on $174,000 gains; by the end of 1968 – Buffett’s first full year of ownership – it was sitting on $1.76 million.

Thus began Warren Buffett’s love affair with ‘float’. According to Schroeder, “To someone like Buffett, having other people’s money to invest, on which he kept the profit, was catnip.” Unlike his fund structure, he could keep a much higher share of the investment profits. And nor were the funds going anywhere.

A few years ago, researchers at AQR Capital Management attempted to reverse engineer Buffett’s investment performance. They concluded that his public securities holdings outperform his private company holdings and wondered therefore why he bothers with the private companies at all. Tax aside, their hypothesis was that the insurance holdings provide a steady source of financing that allows him to leverage his stock portfolio.

They estimate that the structure allows him to apply leverage at 1.7-to-1.

Tech firms are using their platforms to reverse-engineer banking.

Such platforms cannot do everything a bank does, because they do not have a balance-sheet to sustain lending. A bank’s advantage lies in having deposits to exploit, even if they do not know whom they should lend them to. Tech firms’ advantage is that they know whom to lend to, even if they do not have the funds. So some platforms have decided they would like a balance-sheet. Grab, which is about to go public at a valuation of some $40bn, has acquired a banking licence. If many others took this path banks might remain at the heart of the financial system, though the biggest could be Ant, Grab or Mercado Pago, not HSBC, DBS or Santander Brasil.

Till next time.

The Plan vs. the Process (Source: @visualizevalue)

pelotm TAM:

Hmseholds that may or may not be interested in purchasing a

Peloton product today. but could be interested in the future as households

with broadband internet ard that own or are open to purchasing subscliption

pelotm interest: Households that interest in learning more about at least

one

SAM:

Estimated households that

are interested in purchasing one or rnore current Pebton products at current price

SAM

: Estimated households that are

interested in one or more current peloton products at current

Brand and product awareness drives purchase intent (SAM).

TO date, the vast majority Of our advertising spend has been allocated to Bike.

Bike aided awareness is Tread aided awareness.

We expect Tread SAM to grow significantly as we market new Tread in FY 2021.

U Canada and Gemany•

TAM 2m

95 Million

75 Million

52 Million

20 Million

15M

With 1M global CF subscriptions. we are

penetrated vs. —4X 2019

Accounting for households that purchase 2*

units, 2020 Connected Fitness SAM is

20 Million

representing *43% growth over 14M in 2019

PELOTON")