One Step Up #47

This week, we look at the story of The Order Machine (TOM), YouTube & hypergrowth, logistics & e-commerce, David Rolfe, Fixed Income Lessons in Equities, Apple's M&A strategy + more

One big idea for this week:

How Exchanges Die: The Story Of T.O.M.

If you think owning & managing an exchange seems so easy, you might want to think again.

By 2016, TOM (The Order Machine) had amassed 50% market share in Dutch options and growing, boasted powerful owners including Nasdaq, Optiver and ABN AMRO, and was eyeing global expansion. Spectators were calling TOM the victor of a new Battle of the Bund, remembering the dramatic shift of market share in Bund futures from LIFFE to Deutsche Borse. The EU government had given TOM its blessing, allowing it to trade new markets & promote competition on the continent. Everything a winning exchange could want, TOM had.

A year later, TOM was dead.

Key lessons:

Don’t forget the downside and always stress test your ideas

Look at the prices and sentiment

What really causes a company to file for bankruptcy is not leverage per se, but the inability to meet its obligations.

Focus on the Maturity Wall

“Predictable income streams are much more valuable than volatile ones. Cause you can leverage them…” — John Malone

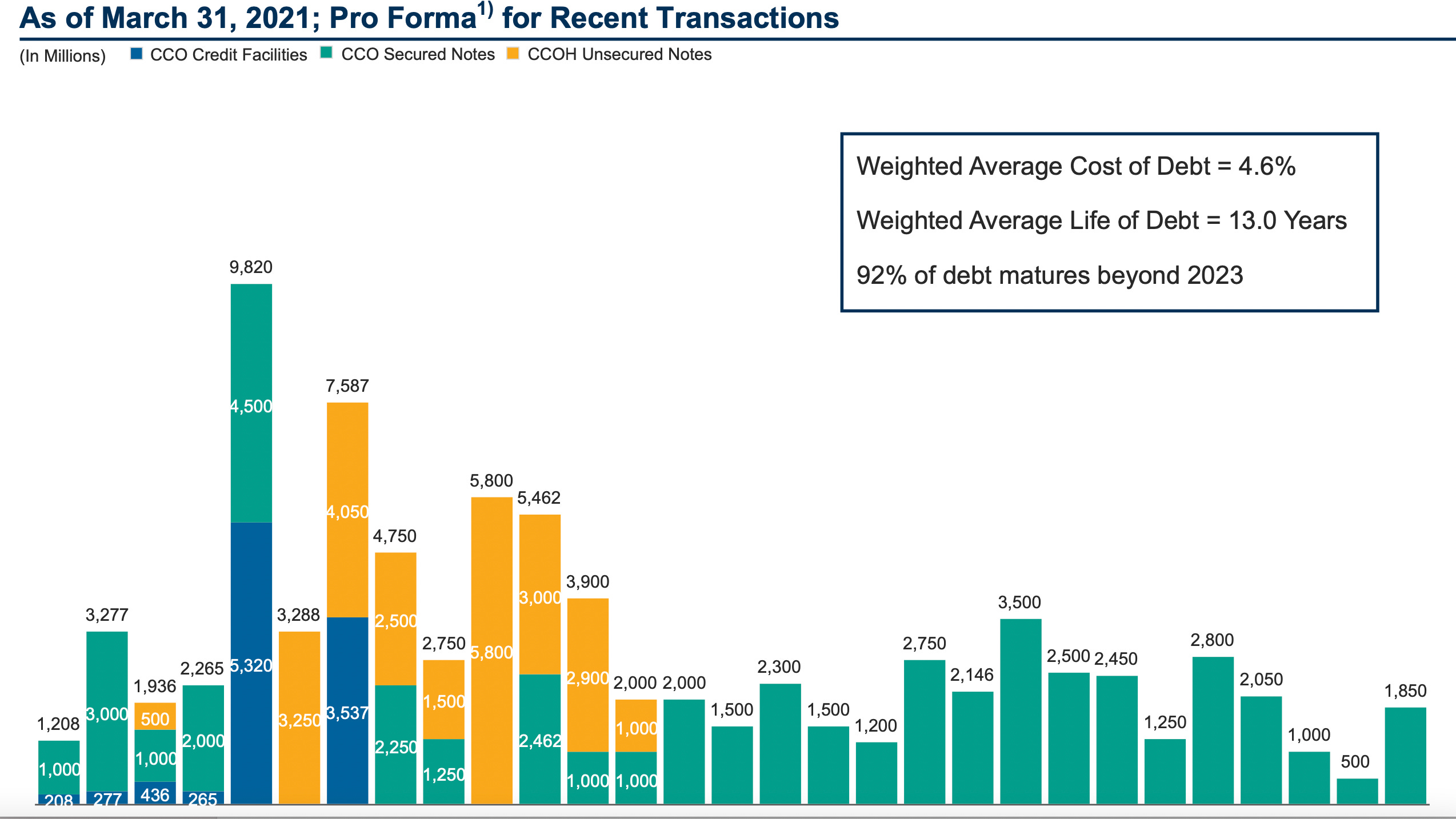

It’s no secret that John Malone is an expert and proponent of leverage. Charter, the second largest U.S. internet cable provider (which he owns part of), is no exception.

Charter’s leverage ratio (Total Debt/EBITDA) is ~4.5X, which may sound high to some people and in fact it’s a High Yield rated company. But let’s take a look more closely at their maturity wall:

We can make two quick observations (assuming you know the company):

The debt is spread out pretty nicely, weighted average maturity is 13 years

Charter generates around $7-8B of predictable free cash flow which comfortably covers all of the upcoming maturities in the next 4 years, and likely will cover 2025 maturities (because it’s growing), also giving them plenty of time to refinance well ahead of the maturity date.

Such a good article. One of my favorite takeaways: Your belief in the long run isn’t enough. Your investors, coworkers, spouses, and friends have to sign up for the ride.

But the greatest companies aren’t an idea, they’re an idea machine.

To be an idea machine, you have to invest in the machinery to deliver ideas. Bill Gates attributes Microsoft’s early success not to its operating system, but to the allocation of a third of its software engineers to build tools for the other two thirds.

An idea machine also invests in its idea-generating capacity. A great company’s deepest innovation isn’t in its product but in its being: a deeply idiosyncratic approach to hiring and working, accumulated through a million tiny acts of discipline and bizarre decisions, which alienates most outsiders, but draws a few in with the special, strange intensity of a children's story, as if it had been made forthem alone.

An inside look (processes, culture) at how YouTube scaled from million of users and revenues to billions.

Diversify by Business Model:

We contend focused investing doesn't have to be risky if you stick with higher quality companies, however, we think a more intelligent way to diversify is to diversify by business model. So obviously Progressive has nothing to doing with Apple in terms of their business model. We're not going to own four or five semiconductor companies, we're not going to own four or five medical device companies. We've been a long-term investor in Visa. We've never owned MasterCard at the same time, because our thinking is those business models - there are some differences on the debit side of things - but they're alike enough that if something goes wrong with Mastercard it is unlikely that Visa escapes unharmed. So the last thing we want in our portfolio is when we make our inevitable mistakes, we don't want pin action in other parts of the portfolio.

The internet matching machine is fuelled by content. The more of it you produce, the more likely you are to reach the people who'd value what you have to offer. Writing a tweet or uploading a video costs nothing. It might be embarrassing or a waste of time, but that’s about it. In that sense, the downside of playing the game is indeed limited.

But focusing on the risks within the game obscures a much bigger problem: The game is no longer optional. Everyone must play. We have little to lose because we already lost everything: Stable jobs, affordable homes, education that lasts a lifetime, and worry-free retirement are no longer an option. Even money itself ain’t what it used to be. It loses value by simply sitting in the bank.

How Apple does M&A: Small and quiet, with no bankers

100 deals over the last 6 years - or, an acquisition every 3 to 4 weeks.

While big tech rivals routinely strike multi-billion dollar deals, Apple has followed a different strategy. It’s refined the “acquihire,” or strategic purchase of a small company primarily for its staff.

Cook said in an interview with CNBC in 2019 that the company’s approach is to identify where the company has technical challenges and then to buy companies that address them. One example was the acquisition of AuthenTec in 2012, which led to the iPhone’s fingerprint scanner. “We bought a company that accelerated Touch ID at a point,” Cook said.

150 Years of US Stock Market Performance as Measured by the S&P 500 Index

See in the link above what long term really looks like.

Speculation: A Game You Can’t Win

Anything with the allure of an astronomical return within a short timeframe isn’t worth the mental (and moral) tension that comes with it. When I invest in things, I do so with a long time horizon so market timing is not a consideration.

Till next time.

We judge ourselves by what we feel capable of doing, while others judge us by what we have already done.

- Henry Wadsworth Longfellow

If you liked this edition, please share it and hit the subscribe bottom below for receiving future editions!